Asset Allocation: Overlook at Your Peril

January 31, 2022 | By Candace Groth

Imagine your business is being purchased for millions of dollars in an asset sale. And almost all of the legal negotiation points have been wrapped up in the Purchase Agreement. And then your attorney, or perhaps your CPA, brings up the “Asset Allocation.” Part way through, your eyes start to gloss over from all the tax speak. “Isn’t this a minor point?” you think. “So minor in fact that the Buyer wants to address it after closing?” This is a bad decision. This blog post explains why the asset allocation matters, whether you are a buyer or a seller, and why this critical issue should not be an afterthought for the post-closing period.[1]

What is the Asset Allocation?

Firstly, and very importantly, the asset allocation only arises as an issue in an Asset Purchase transaction or certain types of Stock/Equity Sales that are treated like an Asset Purchase for tax purposes. [2]The Asset Allocation is, simply put, the amount of the purchase price that is “allocated” or attributed to each individual asset (or usually, groups of assets) being purchased by the Buyer. For example, the Buyer may purchase 10 computers worth $1,000 each for $10,000.

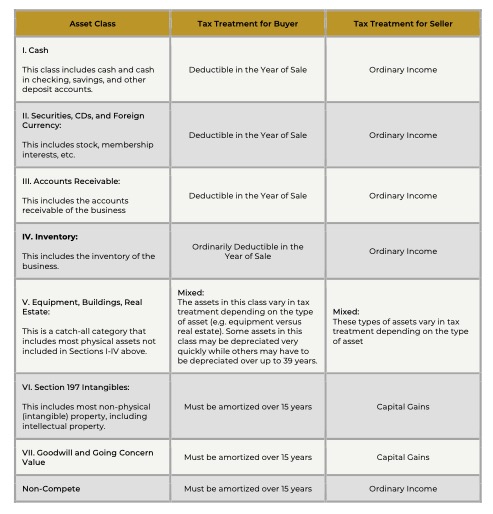

The Internal Revenue Service requires that the Buyer and Seller reflect the allocation on Form 8594 and use the allocation consistently moving forward. Form 8594 breaks the types of assets of the business into seven categories. A brief description of each is listed below[3].

Click the image to enlarge.

Why does the allocation matter?

The allocation is very important for both the Buyer and Seller because it impacts (a) how the transaction will be taxed for the Seller and (b) the Buyer’s ability to speedily depreciate or amortize the assets purchased.

As you might expect, there is a bit of push and pull regarding the different allocations, with an allocation of purchase price that is favorable to the Seller usually being less favorable to the Buyer, and vise versa. Asset allocations for a technology rich startup with few physical assets tend to be very seller friendly; but asset allocations for an inventory heavy business (e.g., a toy manufacturer) will tend to be more buyer friendly.

Earnouts

Transactions that contain an earnout can make the asset allocation even more complicated. An earnout is a post-closing payment, usually contingent on certain economic or other milestones being hit by the business being sold post-closing. For example, an earnout may provide that the seller receives an up to $100,000 payment each year for 3 years, provided that the business hits $4.5M in EBITDA each calendar year.

Earnouts that are very contingent on unknown financial conditions post-closing are often (but not always) treated as ordinary income to the Seller, and deductible to the Buyer. However, sometimes the parties will choose to treat the earnout payments in the same manner as the rest of the purchase price or using a different methodology. Failing to specify how the earnout will be taxed is a common error we see in transactions, particularly for sellers, and one with significant tax consequences.

Asset allocations may not be top of mind when the business owners are excited to exit and start their best and greatest new venture. But the business neglects this critical topic at its own peril. That is why it is critical to consult with an attorney who is comfortable with asset allocations and knowledgeable about merger and acquisition transactions generally, to be sure you get them right. Hopefully, this post will help you understand the asset allocation and provide a starting point for consideration of this item in the context of the larger sale transaction.

[1] Please keep in mind that this post provides only general information. You should consult a CPA or tax professional for additional information about your unique tax situation.

[2] These include Section 338(h)(10) and Section 336(e) election transactions.

[3] Please note that Form 8594 and its instructions describe the asset classes in greater detail.

About the Author(s)

Candace Groth

Candace Groth is a senior attorney at Vela Wood. She focuses on mergers & acquisitions and complex LLC matters.

Learn More